Market Highlights from ANZ Wealth Chief Investment Office

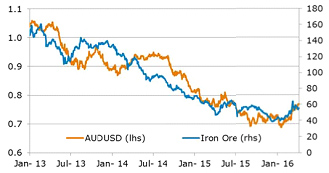

Recovery in China’s construction industry supported higher commodity prices

The AUD rose strongly on declining investor risk aversion

Central banks back in action

Concerns of a sharp deterioration in global growth eased back following three major announcements by central banks in March.

1. The European Central Bank (ECB) –increased the monthly size of asset purchases by €20bn and extended the coverage of these purchases to investment grade non-bank corporate paper. This has significantly reduced risks in the European banking sector, a large holder of these securities. With the ECB now buying up these securities and providing cheap funding to banks, the risk of a more significant slowing in euro zone growth, via a sharp reduction in bank lending, has been greatly reduced.

2. The US Federal Reserve (Fed) – at its March meeting lowered the path of future rate hikes and signalled a reluctance to raise interest rates further on weaker global conditions and still low inflation.

3. China stimulus – following from the National People’s Congress, Chinese authorities boosted credit growth and this is providing genuine support to the industrial sector through a lift in residential construction.

Economic data provided some assistance to the rebound in markets with business surveys pointing to some recovery in US manufacturing following recent weakness. Employment growth has also remained strong. However, indicators point to a softening in growth in the US outside of manufacturing. Analysts have revised down their forecasts for growth in the March quarter following weak orders of capital goods and softer data on consumer spending.

In Australia, the unemployment rate fell back to its recent low point of 5.8%, with this reflecting earlier strong employment growth and a fall in the number of people looking for work. That said, indicators of future employment are showing signs of softening as retail spending softens and housing construction, which has been a bright spot, looks set to wane as approvals to build new homes decline and price growth slows across Sydney and Melbourne.

Shares

Global developed share markets rose by 5.3% in US dollar (USD) terms in March on central bank stimulus. The US led the pack with returns up 6.6% as Fed comments saw markets further reduce expectations for rate rises over the next three years.

European and Japanese markets were up 2.7% and 3.8% respectively as the recent rise in their currencies was perceived to impact earnings.

The Australian share market rose 4.8% led by the resources sector which performed well on higher commodity prices. Returns in the industrial sector of the market were constrained due to the impact of the higher Australian dollar (AUD) as well as concerns over a possible rise in bad debt provisioning in the banking sector.

Iron Ore and Australian Dollar

Source: Bloomberg, ANZ Wealth

Emerging market shares significantly outperformed developed shares, up 13.0% in USD terms. Half of this increase was attributed to the strong rally in emerging market currencies. Chinese stimulus has also helped to ease investor concerns about a ‘hard landing’ and provided support for commodity prices. That said, excess leverage across the region is a point of concern in an environment where the Fed is still set to tighten interest rates, albeit gradually.

Bonds

Better investor sentiment resulted in a rise in most global government bonds during the month. Even so, yields remain at a low level given the softening in global growth and lower inflation expectations. US 10-year yields rose by four basis points (bps) to finish at 1.8%, while European periphery bonds yields fell on ECB policy measures.

Conditions across credit markets generally improved in the month as the bounce in commodity prices helped reduce the likelihood of corporate defaults in the high yield market and the energy sector. Across investment grade corporate bonds central bank stimulus continued to support investor interest. This underpinned a strong return from corporate bonds, which saw a 0.9% return from global fixed income in March. Australian fixed income underperformed its global counterparts as better domestic growth saw Australian 10 year yields rise to 2.5%.

Currencies

Increased investor confidence has seen broad based weakness in the USD and other ‘safe haven’ currencies as investor risk aversion declines. In addition, the USD fell against most major currencies following the more cautious stance of the Fed with regard to future rate rises. The AUD jumped 7.2% while the NZD rose 4.8% given higher commodity prices. This negatively impacted on unhedged returns this month.

Implications

Measures from central banks and stimulus from China has helped ease investor nervousness and provided temporary relief to markets. That said, in our view concerns over the growth outlook are likely to weigh on markets in the medium term. We continue to hold a cautious approach in our asset allocation strategy, with expectations for continued volatility to persist.

While the path of US rate rises has slowed the risks to the US economy, at this stage of the cycle we still see a sufficient upward move in bond yields to impact returns. In Australia, we think that the risks remain skewed towards a decline in central bank cash rates as the drag from mining investment persists at a time when the housing market also cools down. The AUD is expected to weaken further as commodity prices remain sluggish in this lower growth environment.

Major asset class performance as at 31 March 2016 (%)

Source: JP Morgan & ANZ Global Wealth

Indexes: Australian Shares – S&P / ASX300 Accumulation, Global Shares (hedged/unhedged) – MSCI World ex Australia, Global Emerging

Markets – MSCI Emerging Free Net in AUD (unhedged), Global Small Companies (unhedged) – MSCI World Small Cap exAustralia, Global Listed Property – FTSE EPRA/NAREIT Developed, Global Listed Property – FTSE EPRA/NAREIT Developed Rental Index exAustralia (hedged) with FTSE EPRA/NAREIT Developed Index ex Australia (hedged) used before April 2015, Cash – Bloomberg Bank Bill, Australian Fixed Income – Bloomberg Composite Bond All Maturities, International Fixed Income – Barclays Global Aggregate Bond Index (hedged).

Please note: Past performance is not indicative of future performance

Leave A Comment