Dr Shane Oliver is Head of Investment Strategy and Economics and Chief Economist at AMP Capital is responsible for AMP Capital’s diversified investment funds. He provides economic forecasts and analysis of key variables and issues affecting, or likely to affect, all asset markets. In this article ge reviews the economic outlook for 2016.

Asset class views

| Short term (next few months) | Medium term (next 1-3 years) | |

|---|---|---|

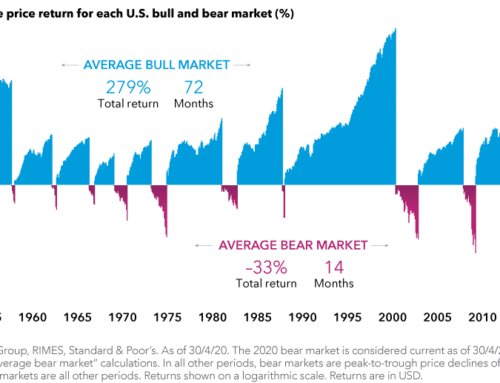

| Global equities | Expect volatility to remain high into the US Federal Reserve’s December meeting, followed by seasonal strength. | The cyclical bull market likely has further to go due to attractive valuations against bonds, ‘not too hot/not too cold’ global growth, a lack of investor euphoria and easy monetary conditions but we remain vigilant to any deterioration in fundamentals. |

| Australian Equities | Expect volatility to remain high into the US Federal Reserve’s December meeting, followed by seasonal strength. | A continuing cyclical bull market globally and low interest rates, the boost to profits from a lower Australian dollar and a gradual rebalancing in economic growth will help drive the market higher. However, the end of the commodity super cycle likely means Australian shares will remain relative underperformers globally. |

| Government bonds | We expect bond yields to gradually rise as the US economy continues to grow and the US Federal Reserve moves to gradually raise interest rates. Valuations remain stretched. | Low starting point yields mean low expected medium-term returns. However, bonds retain their diversification value. |

| Corporate bonds | Credit spreads have widened with growth worries and concerns about energy companies. This looks overdone. | Credit valuations are around neutral, but are reliant on low bond yields. |

| Property & Infrastructure | Property and infrastructure assets are likely to see ongoing support from the search for yield. | Higher-yield assets should do well over the medium term helped by low bond yields. The main threat would be a sharper-than-expected back-up in bond yields. |

| Commodities | Commodities have become oversold and could bounce higher in the months ahead. | While the secular forces of rising commodity supply are a negative, there is potential for a cyclical rally as the global economic expansion continues and valuations are now attractive for many commodities. |

| Currencies | The US dollar could well peak around the time of the potential first US Federal Reserve rate hike in December as the markets ‘buys the rumour and sells the news’. | The Australian dollar is likely to continue to trend down to $US0.60 or lower due to poor fundamentals. |

Leave A Comment